Will the Federal Reserve Interest Rates Impact Oil and Gas, Quality of Life

Will the Federal Reserve Interest Rates Impact Oil and Gas, Quality of Life

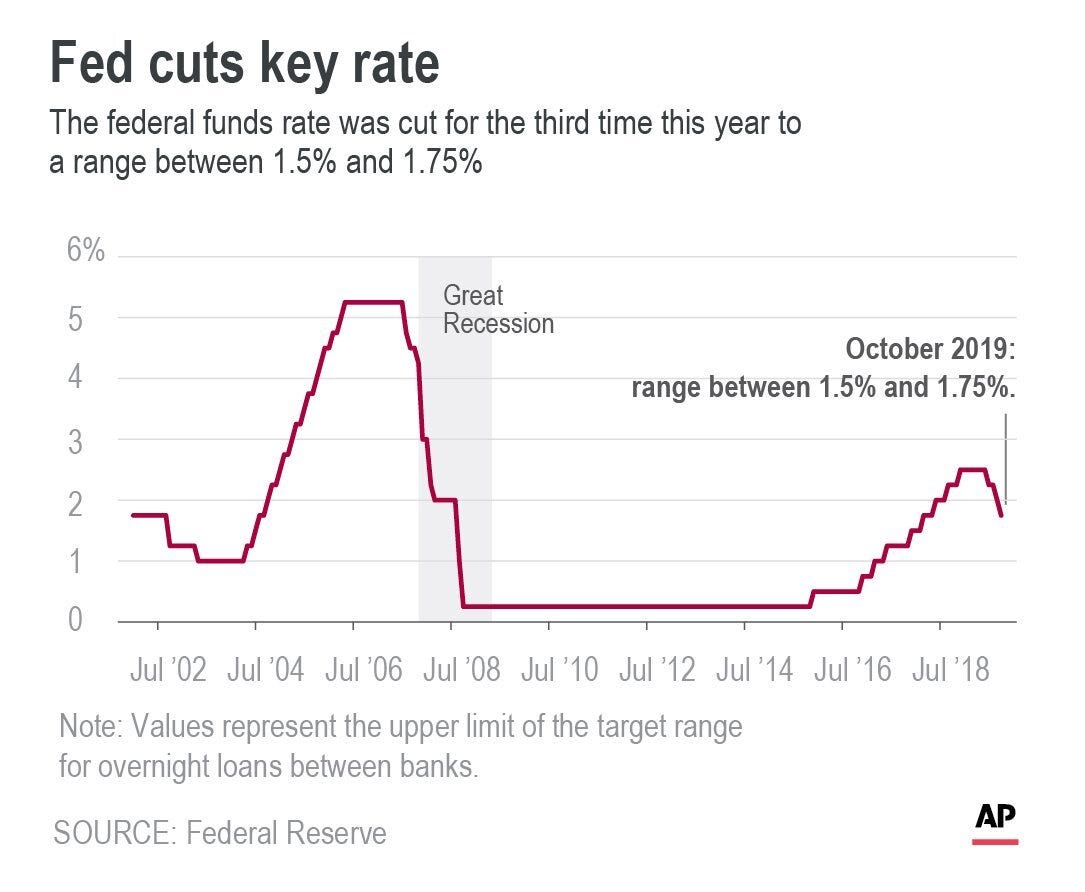

When the Federal Reserve (Fed) cuts interest rates, it typically aims to stimulate economic activity by lowering the cost of borrowing, which can influence oil and gas development.

The history of Federal Reserve interest rate cuts has been marked by a dynamic relationship between monetary policy and economic performance. When the Federal Reserve (Fed) cuts interest rates, it typically aims to stimulate economic activity by lowering the cost of borrowing, which can influence corporate profits, small businesses, mortgage activity, and the overall quality of life for families.

Here's a breakdown of how Fed rate cuts affected oil and gas companies across 3-month, 9-month, 18-month, and 36-month timelines:

3 Months:

Immediate Effects: A Fed rate cut typically lowers borrowing costs, increasing liquidity for businesses. In the oil and gas sector, this could mean easier access to capital for exploration and production, but immediate market reactions can be mixed.

Oil Prices: Lower interest rates can weaken the U.S. dollar, potentially increasing oil prices as crude is traded globally in dollars. Higher prices may boost revenues short term [3].

9 Months:

Investment Growth: By this time, lower interest rates often encourage more significant investments in capital-intensive sectors like oil and gas. Companies might increase drilling and production due to lower borrowing costs.

Demand Impact: As economic activity picks up, demand for oil and gas may increase, supporting higher prices and company revenues [1].

18 Months:

Expansion and Volatility: Fed rate cuts after this period may lead to increased expansion within the oil and gas industry. However, volatile energy prices and potential inflationary pressures from an overheating economy can also emerge. Supply chain costs may rise, affecting profitability [6].

36 Months:

Long-Term Growth or Overheating: Over the long term, persistent low rates may cause inflation, which could raise operational costs for oil and gas companies. On the other hand, sustained economic growth boosts energy demand. However, if the economy overheats, the Fed may raise rates again, reducing liquidity and dampening growth prospects

Beyond oil and gas, the supply chain and communities can be impacted as well. The impact of these rate cuts can be observed by revealing a varying degree of influence on the economy.

1. The Immediate Impact: 3 Months Post-Rate Cut

In the first three months after a Federal Reserve interest rate cut, the effects tend to be limited primarily to financial markets and immediate lending sectors. Rate cuts reduce the cost of borrowing for banks, which then pass on lower interest rates to consumers and businesses. Here are some key impacts during this period:

Corporate Profits: In the short term, corporations may benefit from lower borrowing costs, especially for those reliant on short-term loans. These reductions in interest expenses can provide a modest boost to profitability, particularly for highly leveraged companies.

Small Businesses: For small businesses, reduced interest rates can make borrowing more affordable, allowing them to expand operations or maintain liquidity. However, the immediate impact is often muted because small business owners may not have quick access to new loans or may be cautious about expanding during times of uncertainty.

Bank Loans: Banks may start offering more attractive terms on loans, but many businesses and individuals are often slow to react in the short term. The three-month window often shows only a slight uptick in lending activity.

Mortgage Activity: Mortgage rates, which are closely tied to interest rates, often see an immediate decline after rate cuts. This can result in a temporary spike in mortgage refinancing and a slight increase in home purchases, although it typically takes longer for significant changes to housing markets.

Quality of Life: For families, the immediate impact is generally limited. While lower mortgage rates may offer some homeowners an opportunity to refinance, the broader effect on household spending and disposable income tends to be minimal in the short term.

2. The Medium-Term Impact: 9 Months Post-Rate Cut

By the 9-month mark, the effects of an interest rate cut become more pronounced, as businesses and consumers adjust to the new economic conditions.

Corporate Profits: With more time to adjust, corporations often see larger gains. Companies that rely on debt financing may experience increased profitability as their cost of capital declines. Consumer-facing companies, especially in the housing and automotive sectors, may see rising demand as lower interest rates spur spending.

Small Businesses: Small businesses may now be more likely to borrow and invest in growth. Lower interest rates mean that loans for capital improvements, inventory expansion, or hiring become more affordable, leading to a more visible positive impact on the small business sector.

Bank Loans: Lending activity typically increases by this stage. Banks, encouraged by lower rates, may see more demand for personal, auto, and business loans. Additionally, credit conditions for consumers may improve, allowing more individuals to access credit.

Mortgage Activity: By the 9-month mark, the housing market may experience more noticeable changes. Homebuyers take advantage of lower mortgage rates, leading to increased home sales and refinancing activity. This period often witnesses an uptick in home construction and related industries.

Quality of Life: For families, the improvement in economic conditions may start to feel more tangible. With lower rates, families can refinance mortgages, take out cheaper loans, or reduce debt burdens. Increased hiring by businesses also creates more job opportunities, leading to greater income stability and consumer confidence.

3. The Long-Term Impact: 18 Months Post-Rate Cut

After 18 months, the full effects of interest rate cuts generally become apparent across the economy, often signaling a significant period of economic growth or recovery.

Corporate Profits: Corporate profits tend to show strong improvement. Companies that have borrowed at lower rates may now see the return on their investments in growth and expansion. Consumer demand often rises due to higher employment rates and lower borrowing costs, further boosting corporate revenues.

Small Businesses: The environment for small businesses improves as well. With increased demand for goods and services, small businesses are better positioned to grow, hire more employees, and invest in new opportunities. Banks are more willing to extend credit as the economy shows stronger signs of recovery.

Bank Loans: Loan growth often peaks during this period as consumer confidence grows and banks offer favorable terms. Increased lending in areas like auto loans, business loans, and mortgages indicates that the economy is in a more robust phase of recovery or growth.

Mortgage Activity: The housing market may enter a period of sustained growth. Home prices often rise as demand increases, fueled by lower mortgage rates. Refinancing activity may also reach its highest point during this time, as homeowners take advantage of prolonged low rates.

Quality of Life: For families, this is typically the period where the benefits of lower interest rates are most strongly felt. Lower unemployment, increased consumer spending, and higher disposable income contribute to a noticeable improvement in the quality of life. However, rising home prices can make affordability an issue for new buyers.

4. The Extended Impact: 36 Months Post-Rate Cut

At the 36-month mark, the long-term effects of interest rate cuts can reveal both positive growth and potential challenges, particularly in cases where the economy may begin to overheat.

Corporate Profits: Corporate profits may continue to rise, although the pace of growth could begin to moderate as businesses face higher input costs due to increased demand and inflationary pressures. Some sectors, like technology and real estate, may show outsized growth due to prolonged access to cheap credit.

Small Businesses: Small businesses generally enjoy a stable environment, with greater access to capital and sustained consumer demand. However, those reliant on cheap credit may begin to feel the effects of rising inflation, and some may struggle if the Fed decides to reverse course and raise interest rates.

Bank Loans: Lending activity may start to slow as the economy enters a more mature phase of the business cycle. Banks could tighten lending standards in response to inflation concerns or the anticipation of future rate hikes.

Mortgage Activity: The housing market may start to experience signs of cooling, especially if home prices have risen to unsustainable levels. Higher home prices can deter new buyers, and the Fed may begin to reverse rate cuts if inflation becomes a concern, making borrowing more expensive.

Quality of Life: For families, the long-term benefits of rate cuts may begin to diminish as inflation rises, reducing purchasing power. While wages may rise, they may not keep pace with inflation, leading to higher costs of living. Families that have already refinanced mortgages or taken out loans may benefit, but new borrowers may face higher prices and interest rates.

Conclusion

The history of Federal Reserve interest rate cuts shows that their impact unfolds over time, influencing various aspects of the economy. In the short term (3 months), the effects are mainly limited to financial markets and early stages of lending. Over a 9-month period, borrowing and investment activity increase, leading to broader economic gains. By 18 months, the economy generally experiences robust growth, with corporate profits and consumer spending rising.

However, by the 36-month mark, potential risks such as inflation and overheated markets may emerge, requiring the Fed to reassess its monetary policy stance. Throughout these phases, corporate profits, small businesses, bank loans, mortgage activity, and families’ quality of life are all shaped by the broader economic environment fostered by rate cuts.

CLICK HERE FOR SPECIAL DISCOUNT LINK

Half the price, all the fun. Get 50% OFF any Paramount+ annual plan for a limited time! Take advantage of the fall offer and start streaming...

Take advantage of this limited time offer and stream the NFL on CBS live on Paramount+. Redeem now!

Everyday your story is being told by someone. Who is telling your story? Who are you telling your story to?

Email your sustainable story ideas, professional press releases or petro-powered podcast submissions to thecontentcreationstudios(AT)gmail(DOT)com.

#thecrudelife promotes a culture of inclusion and respect through interviews, content creation, live events and partnerships that educate, enrich, and empower people to create a positive social environment for all, regardless of age, race, religion, sexual orientation, or physical or intellectual ability.

MORE FROM THE CRUDE LIFE

Please click that ♡ button, share, and subscribe.

Please share the links on social media.

Thank you thank you thank you for your engagement and support.

If you have a news tip, press release, guest suggestion or other content concepts, please email thecontentcreationstudios(AT)gmail(DOT)com

This post was brought to you in part by one of The Crude Life’s fantastic sponsors, please consider supporting their services or learning more about their organization by clicking on the banner below.

Witting Partners

Witting Partners helps energy industry leaders achieve and sustain peak performance by combining an unmatched blend of oil & gas experience, insight, and results with the power of leadership coaching, workshops, and keynotes so that you and your stakeholders don't un-wittingly damage your odds of achieving long-term success.

If you want to produce 𝑺𝑼𝑺𝑻𝑨𝑰𝑵𝑨𝑩𝑳𝑬 results, then turn to a resource with 15+ years of proven success stretching from the Gulf of Mexico to Appalachia, from service company to operator, and from drilling rig to downtown boardroom.

To learn more, visit Witting Partners’ website or follow on LinkedIn.